Product preview

The apps your customers will actually use.

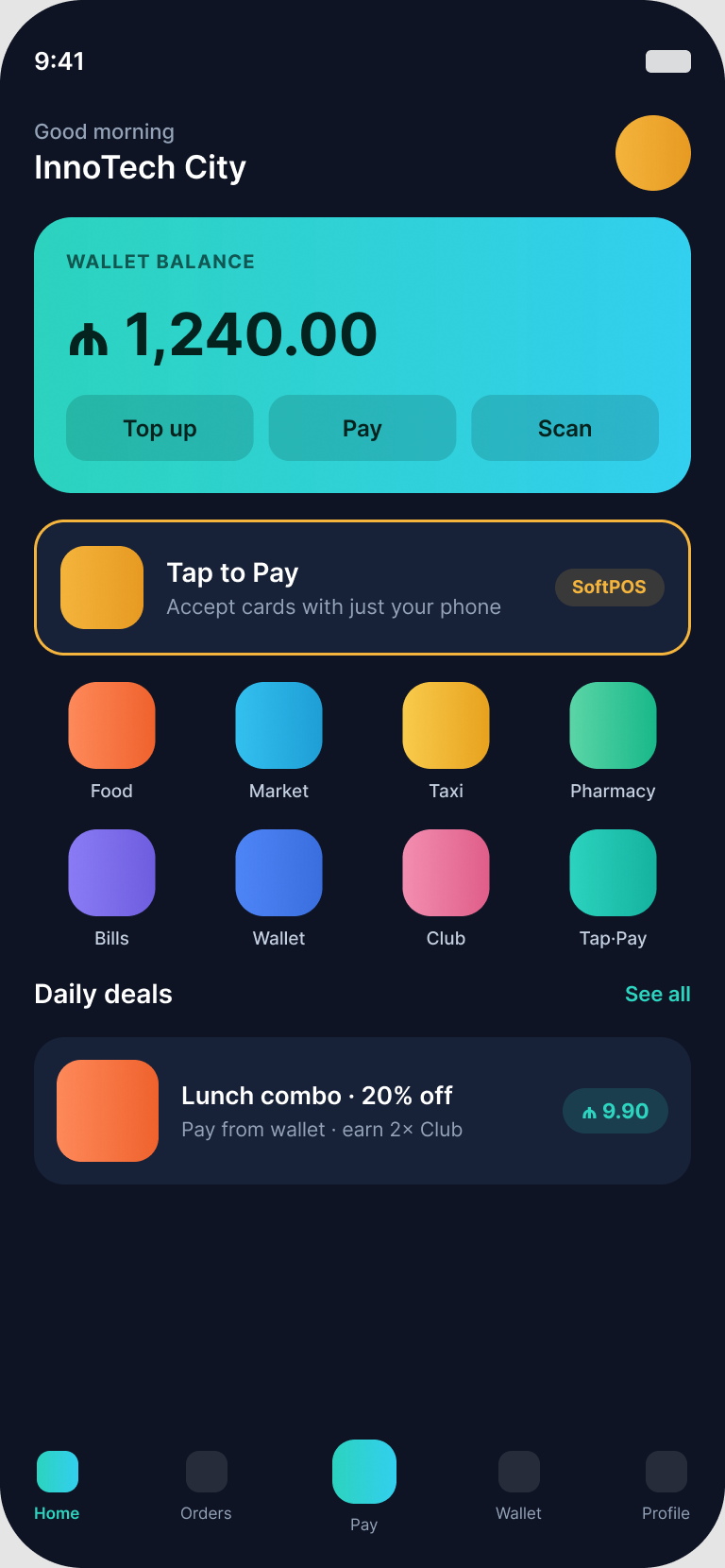

A polished, fully white-labelled consumer app — your brand, your colours, your modules. Tap to Pay turns any phone into a card terminal.

A complete, white-label platform — wallet, commerce, loyalty and core-banking on one set of rails. Deploy it for your own company, or take the technology and build the business in your market. Cloud or on-prem.

A voucher provider, a delivery app, and a bank — three contracts, three reconciliations, and no single book of record. The money moves, but nobody owns the ledger underneath it.

Want governed, tax-advantaged staff benefits — but must glue a voucher vendor to a delivery app to a bank, with no unified spend control or book of record.

Accept fragmented closed-loop vouchers with no marketplace demand attached and no operator system to actually run the venue, inventory or staff.

Carry the licence and balance sheet but ship product slowly, can't use pure cloud for core processing, and have no behavioural data to underwrite on.

A control plane mints tenants and sets policy bounds. A gateway routes each tenant in isolation. A commerce backend and a double-entry ledger book every transaction — and the same money chain powers food, grocery, hotel, pharmacy and 18 more verticals.

Most “embedded fintech” rents a third-party engine and just routes money. This platform owns the ledger the whole super-app runs on, wraps it in white-label multi-tenancy, and ships it self-hostable.

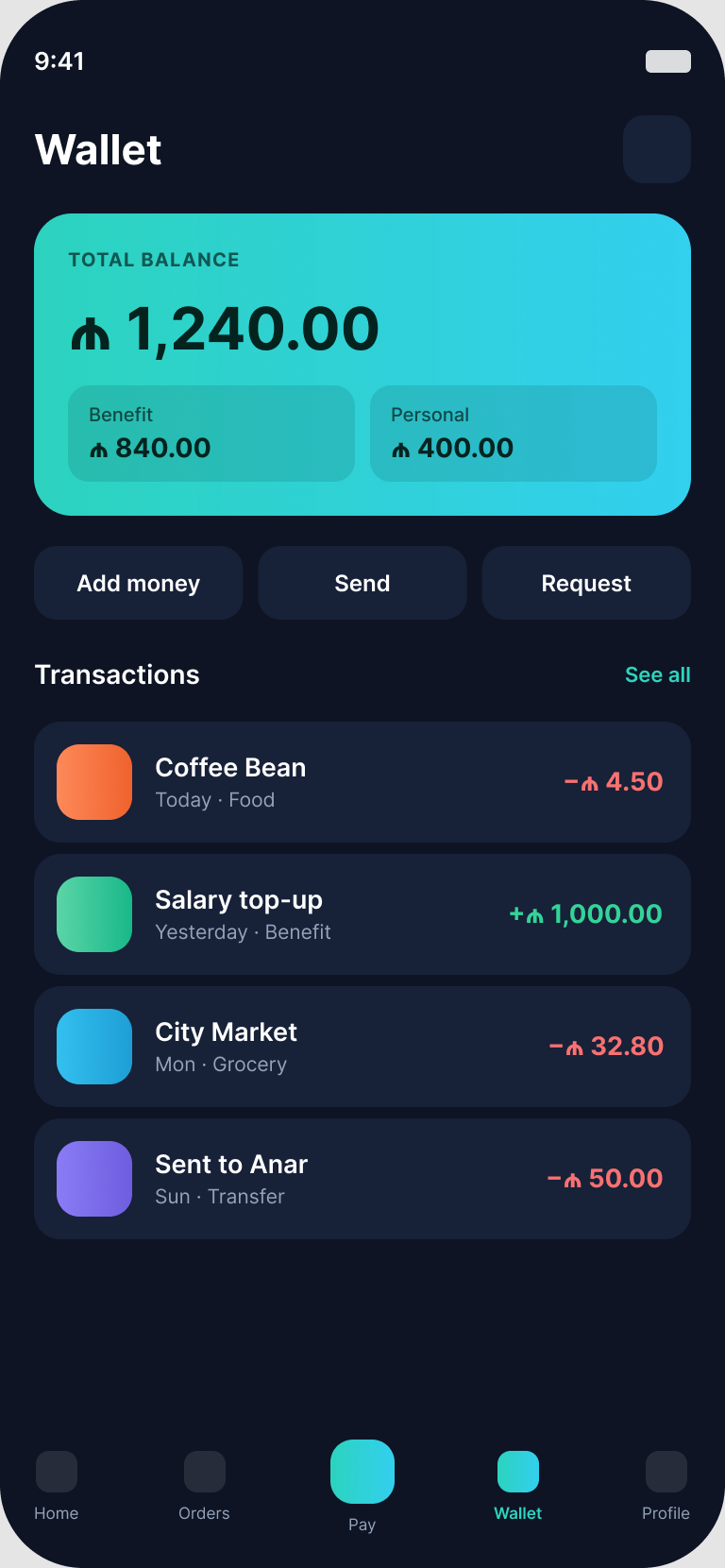

A closed-loop, double-entry core-banking ledger — the money source of truth. You keep the payment economics; there's no engine-vendor tax on every transaction.

One platform, unlimited branded tenants. Provisioning mints a tenant, a branded app, and a banking tenant in a single step — no bespoke code per customer.

Every capability is a toggle. Each tenant enables only the modules it sells, and the app renders exactly that surface — same backend, a different product per customer.

Run it on our managed cloud for speed, or license it on-prem inside your own perimeter — the unlock for banks and regulators who can't use pure cloud.

order → authorize → ledger posting → notification → receipt → fulfilment. The part most demos fake — the books actually balancing — is the part proven first.

Marketplace commission, merchant SaaS, payment fees, BNPL and ads all post to the same ledger. Revenue compounds with volume, not headcount.

A library of composable modules across six categories, plus 22 ready-made business verticals — each reusing the same POS, inventory, payments and ledger spine. Enable per tenant; new verticals are weeks, not quarters.

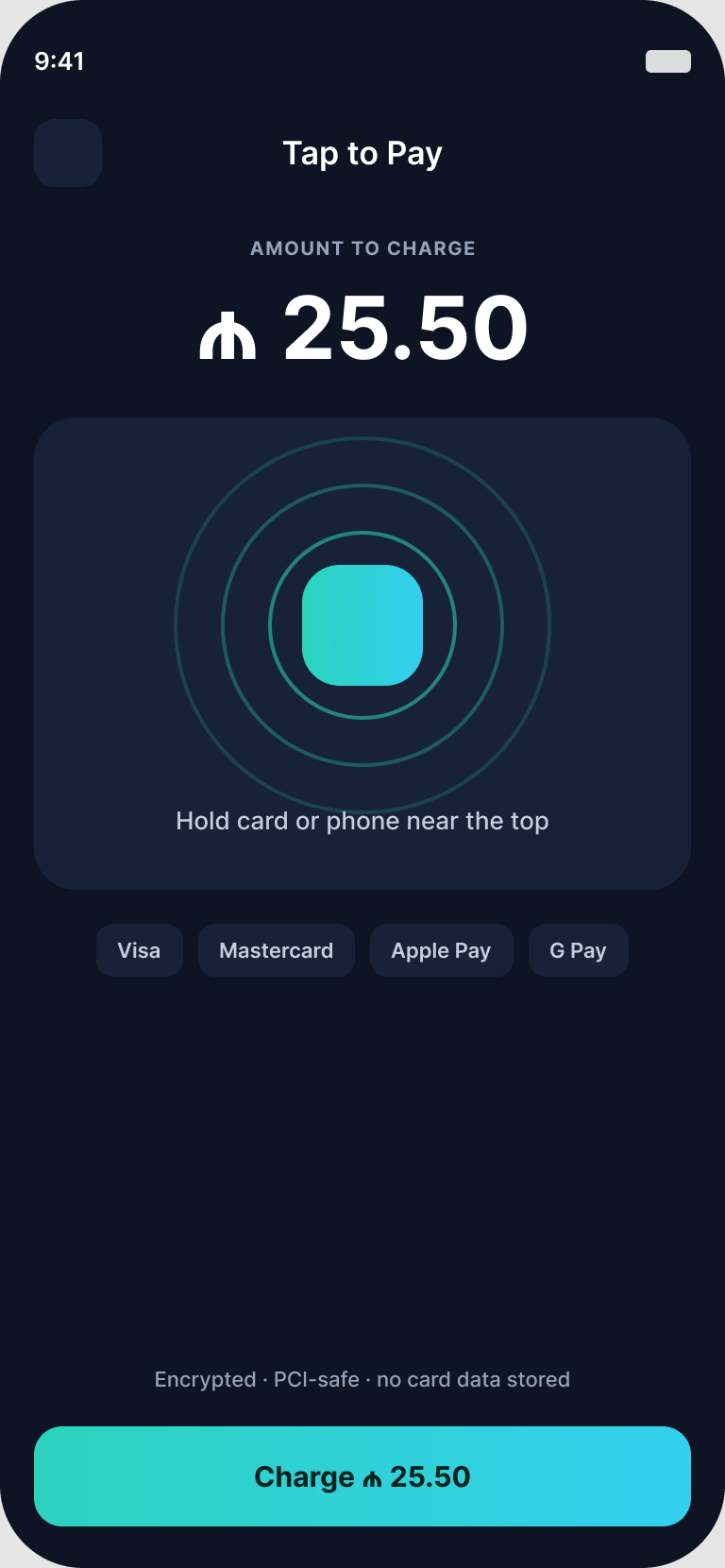

Accept Visa, Mastercard, Apple Pay and Google Pay on a standard phone — no extra hardware. PCI-safe SoftPOS, no raw card data stored. Built in, ready to white-label as yours.

Some of these modules are full products in their own right — operator systems a single business will pay for. Open one to see the functionality inside.

Waiter app, KDS, inventory, procurement, fiscal, payroll, CRM and multi-branch analytics — a full restaurant operating system.

70+ modules · waiter app Open functionalityMulti-branch POS, goods receipt (GRN), FEFO + moving-average COGS, customer credit, returns and inter-branch transfers.

46+ admin screens Open functionalityRooms, bookings, folio settlement, housekeeping, fiscal and guest QR — with Opera / Elektraweb / native adapters.

13+ modules · PMS Open functionalityCustomer super-app, courier app with live GPS dispatch, merchant panel and admin — a white-label, headless food-delivery & courier engine.

4 apps · GPS dispatch Open functionalityRider and driver apps on a real live map — 9 ride tiers, live dispatch, safety, tips and payments. Full Bolt/Uber parity.

9 tiers · live map Open functionalityTurn any phone into a card terminal — Visa, Mastercard, Apple & Google Pay. PCI-safe, no raw card data, no extra hardware.

Phone = terminal On requestDouble-entry ledger, KYB / KYC, holds & payouts, reconciliation and regulatory reporting — the money spine under everything.

FinCore ledger On requestConsumer apps in Flutter (iOS / Android / web); operator and control-plane portals on the web. All on one identity and one ledger.

Wallet, ordering, bookings, loyalty, club and AI concierge.

Fund benefit wallets, set policy within bounds, manage staff.

Orders, menu, inventory, staff, finance, payouts, campaigns.

Mint tenants, set bounds, run the core-banking control plane.

Driver dispatch, route nav; field POS for delivery merchants.

Phone-as-terminal: card, Apple Pay, Google Pay — secure, no raw card data.

Open API reference, webhooks and auth — integrate fast.

Ledger console, gateway admin and KYB / KYC.

A polished, fully white-labelled consumer app — your brand, your colours, your modules. Tap to Pay turns any phone into a card terminal.

The same platform ships two ways — fully managed in the cloud, or licensed on-prem inside your own perimeter.

We host it. Fastest path to a live branded app.

Runs inside your perimeter. The unlock for banks & regulators.

The same technology serves two journeys. Build a private ecosystem for your organization, or acquire the platform and launch a commercial super-app in your market.

A holding or company deploys the whole ecosystem for internal use — staff benefits, a corporate wallet, internal commerce, and resident or guest services — all under your own brand, with one book of record.

An operator or entrepreneur acquires the technology and runs a commercial super-app in their country — onboard merchants, sign up employers and residents, and monetise every transaction across five revenue layers.

Give staff governed, tax-advantaged benefit wallets — food, fuel, pharmacy, family — spendable across a real merchant marketplace, with one book of record.

License the rails, deploy on-prem, and become the distribution channel — pre-onboarded customers, sticky deposits, behavioural data, and a per-tenant core-banking gateway.

A full POS/ERP to run the venue — orders, inventory, staff, fiscal — plus marketplace demand routed straight to your counter and same-day payouts.

A community super-app — apartment management, utility payments, requests, guest QR passes, announcements and a resident club, all in one place.

Hotel + PMS, beach and spa booking, restaurant QR-menu, events and transport — one guest wallet across every point of spend on the property.

Bundle a dozen verticals behind one wallet and one identity — wallet, delivery, mobility, bookings and an AI concierge, ready to white-label for your market.

Zero-trust service auth, unified identity, real fuzzy sanctions/PEP screening and amount-anomaly fraud detection — enforced in the ledger, not bolted on.

The closed-loop ledger and the flows above are deployed and verified. Real-money rails — live card acquiring, a KYC vendor, fiscalization, bank payouts — are interface-ready and go live with your bank/PSP partner and credentials. Strong for a pilot today; a regulated go-live is hardening on an already-correct foundation, not new core engineering.

From the problems it removes to the revenue and loyalty it creates: the business case in four parts.

Employers, merchants and banks otherwise stitch together a voucher vendor, a delivery app and a bank — three contracts, three reconciliations, no single book of record. InnoTechSolution unifies them: every order, payment, payout and refund posts to one double-entry ledger, and a branded app launches in weeks, not years.

One book of record across every vertical and branch; realised margin per sale (moving-average COGS) instead of month-end guesses; live GPS dispatch and tracking; offline-first tills; automated procurement, fiscal/VAT, payroll and reconciliation; an AI concierge and AI booking; and Tap to Pay that turns any phone into a card terminal.

Five GMV-linked revenue layers — marketplace commission, merchant SaaS, payment fees, BNPL and ads — so revenue compounds with volume. Plus white-label resale (run it as your own venture), recurring on-prem licensing for banks and regulators, and a bank profit-share on interchange, float, lending and FX.

For holdings and large employers, payroll and benefits spend becomes engagement: governed, tax-advantaged benefit wallets (food, fuel, pharmacy, family), a Club program with points, tiers (bronze → platinum) and badges, per-category cashback, premium memberships and corporate perks — one app, one book of record, higher activation and retention. Spendable money is kept separate from stat-only loyalty points.

Indicative tiers — every deployment is scoped to your verticals, tenant count and integrations. Talk to us for a quote.

The double-entry ledger and the closed-loop money chain are deployed and verified — that's the hard part, and it's done. The regulated rails (live card acquiring, a KYC vendor, fiscalization, bank payouts) are interface-ready and switch on with your bank/PSP partner and credentials. It's strong for a closed-loop pilot now; a full regulated go-live is sequenced hardening on an already-correct foundation, not new core engineering.

Provisioning mints a tenant, a white-label app and a banking tenant in a single step — then you toggle on the modules you sell. A focused pilot stands up in weeks, not quarters, because every vertical reuses the same POS, inventory, payments and ledger foundation.

Yes. In on-prem mode the whole stack runs on your infrastructure under license. Customer funds, the ledger, KYC and PII never leave your perimeter — the single most important enabler for selling to supervised institutions. Health and license-status checks stay reachable even if the license lapses, so your operators can always diagnose and renew.

We own it. It's our own double-entry core-banking ledger — the money source of truth — so you keep the payment economics instead of paying an engine-vendor tax on every transaction. Local wallet balances are demoted to a cache; the ledger is canonical and reconciles daily.

One backend serves many tenants. Each tenant carries its own brand, data isolation and a module configuration; the app loads a per-tenant config and renders only the enabled modules. Same code, a different product per customer — controlled by configuration, not forks.

The platform is built for Azerbaijan and the wider CIS, with trilingual AZ / RU / EN across the consumer and admin surfaces and regulatory interfaces wired in. The same multi-tenant, self-hostable codebase extends to new markets without a rewrite.

It removes vendor fragmentation. Employers, merchants and banks otherwise stitch together a voucher vendor, a delivery app and a bank — three contracts, three reconciliations, no single book of record. InnoTechSolution unifies them on one double-entry core-banking ledger where every order, payment, payout and refund is booked, and a branded app launches in weeks instead of years.

Five GMV-linked revenue layers — marketplace commission, merchant SaaS, payment fees, BNPL and ads — so revenue compounds with transaction volume, not headcount. Plus white-label resale to run it as your own venture, recurring on-prem licensing for banks and regulators, and a bank profit-share on interchange, float, lending and FX.

For holdings and large employers it turns payroll and benefits spend into engagement: governed, tax-advantaged benefit wallets (food, fuel, pharmacy, family), a Club program with points, tiers from bronze to platinum and badges, per-category cashback, premium memberships and corporate perks — one app and one book of record, with spendable money kept separate from stat-only loyalty points, driving activation and retention.

We'll walk you through the consoles, provision a tenant in front of you, and run the closed-loop money chain end-to-end — cloud or on-prem. Bring your hardest questions.

info@innotechsolution.az · +994 10 220 01 23 · www.innotechsolution.az

Tell us about your project and we'll set up a live walkthrough — cloud or on-prem.